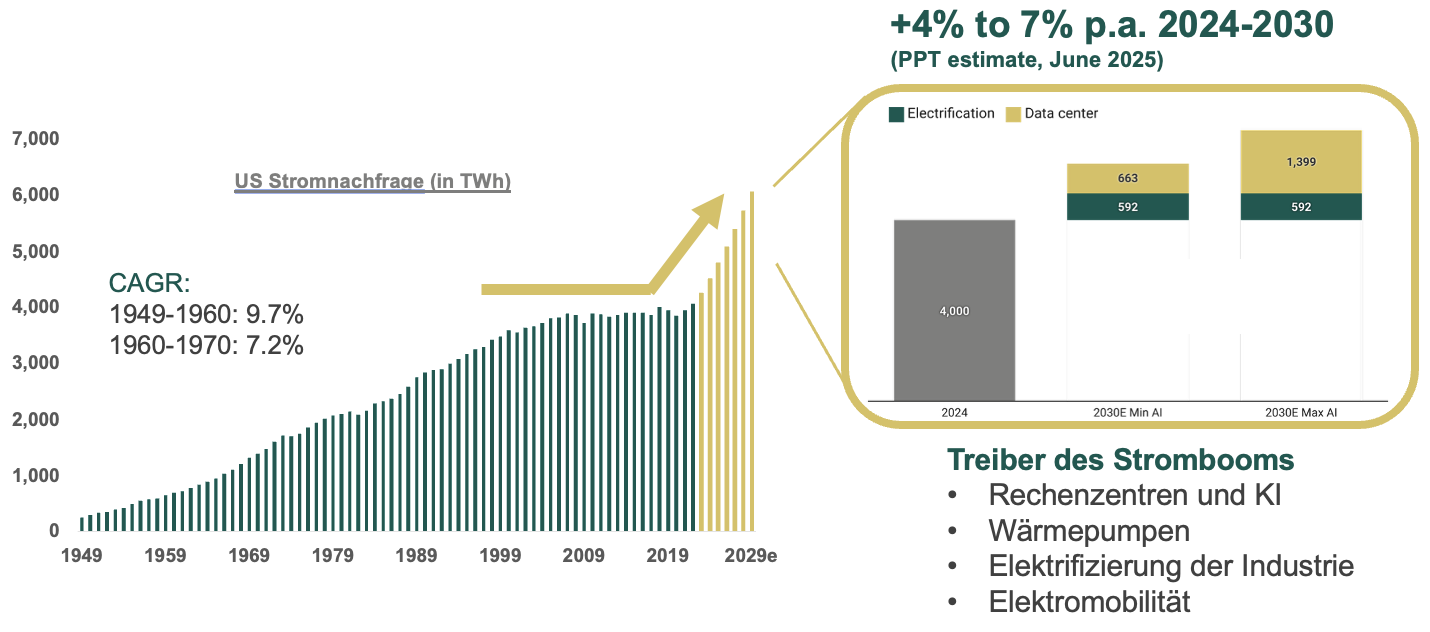

Demand for electricity is a constant. Like Archimedes’ number pi, consumption has hardly changed since 2000. In the US, it stands at around 4,000 TWh (terawatt hours), in the EU at 3,000 TWh and in Switzerland at around 60 TWh.

Technological advances in energy efficiency have kept electricity demand in check over the past 20 years. This has enabled a remarkably smooth transition from coal-fired power to renewable energies. In Germany, the share of renewable energies in the electricity mix has risen from 3% in 2003 to 65% in the first half of 2025. This would have been considered almost impossible at the time, and the seemingly inevitable system crash has not materialised.

Today, remarkable things are happening in the electricity sector. The constant, i.e. demand, is becoming an accelerator.

Prometheus, Hyperion and Stargate

Prometheus, in Greek mythology, is the bringer of fire. The Prometheus of the electricity industry is Meta’s data centre of the same name in the state of Ohio. From 2026, computer chips here will convert up to 1,000 MW (megawatts) of electricity into AI applications and a lot of heat. This will significantly fuel demand for electricity. These facilities run around the clock. To illustrate: 1,000 MW is equivalent to the output of a large nuclear power plant.

At Meta, will be followed Prometheus by the Hyperion project in Louisiana. Hyperion, something like the creator of light in mythology, is expected to require 5,000 MW of power by 2030. The whole project is to be developed at the speed of light. Time is of the essence. In Texas, too, the Stargate project is reaching for the stars. The list could go on and on. Models assume that a total of 89,000 MW will be required for AI applications by 2030. This corresponds to almost the entire output of the 94 nuclear power plants currently in operation in the USA.

Refrigerators, air conditioning systems and data centres

Refrigerators and air conditioning systems were responsible for the last electricity boom in the 1950s and 1960s. Data centres are playing a key role in the electricity boom that is just beginning. We expect electricity demand in the US to grow by 4-7% per year until 2030. These are unprecedented levels.

Next electricity boom in the USA. Source: PPT, Clean Grid Initiative and McKinsey. June 2025.

For the first time in 25 years, electricity demand is growing faster than supply. Neither the electricity market nor investors are prepared for this structural change.

Timeframes and costs

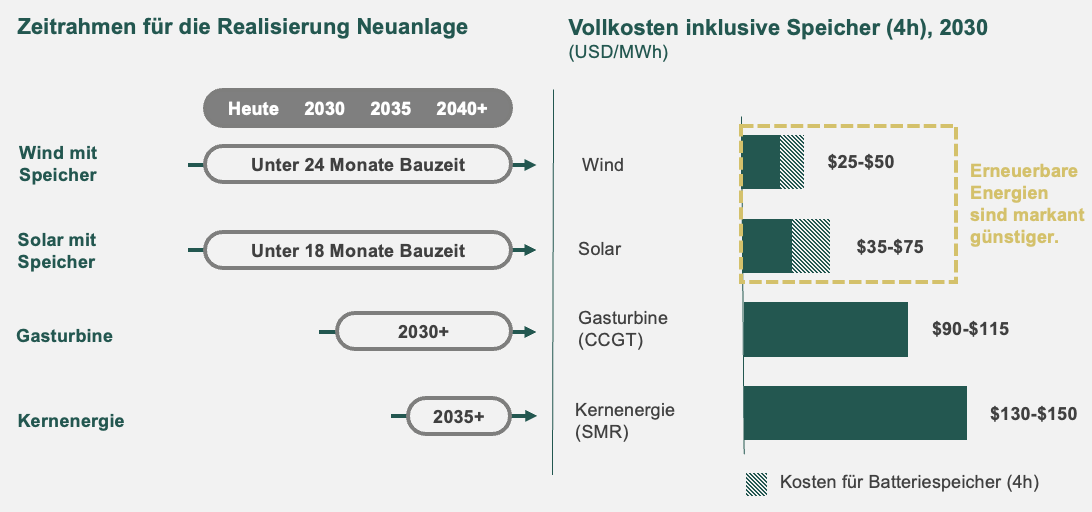

Large-scale projects in hydro, nuclear or gas power take a long time to complete. A new gas turbine will not be connected to the grid before 2030, and new nuclear power plants will not be operational until 2035 at the earliest. Existing gas turbines that are not yet operating at their maximum capacity can only contribute a small portion of electricity production. The majority of the electricity gap must be covered by renewable energy sources.

A shortfall in electricity is much more serious than with other energy sources, as electricity is extremely difficult to store.

Wind and solar power plants with battery storage can be implemented quickly. Contrary to the ‘energy-reactionary’ zeitgeist, most subsidies for renewable energies have survived the ‘One Big Beautiful Bill Act’. However, the speed of implementation is not the only advantage of renewable energies. They are also unrivalled in terms of cost.

Onshore wind power with 4 hours of battery storage can be implemented at 25-50 USD/MWh. Solar power with the same storage costs 35 to 75 USD/MWh. The comparable costs of a new gas-fired combined cycle power plant currently amount to 90-115 USD/MWh. In Iowa and Colorado, the new wind turbines operate at full capacity over 40% of the time and generate electricity at a cost of less than 30 USD/MWh. With storage technology and AI applications in demand management, a reliable electricity supply can be implemented very cost-effectively.

Timeframe and costs of new production facilities. Source: NextEra Energy, August 2025. CCGT: combined cycle gas turbine, SMR: small modular reactor.

Electricity prices will rise significantly. In North America, prices could well double. The price increase overseas will happen faster than in Europe. Demand dynamics are many times stronger. Europe will follow with a delay of two to three years. In Switzerland, too, we will feel the surge in demand from data centres in Volketswil, Rafz and Dielsdorf.

Renewable energies are underestimated and undervalued by the capital market. Even though nuclear energy is once again a hot topic, over 80% of new production capacity will come from renewable energies in the next 5-10 years. In 2024, the figure was as high as 94% in the USA. The capital market has not valued the growth plans of electricity producers, or has even discounted them in relation to investments. This undervaluation offers an attractive entry point today.

New market participants with high willingness to pay. Rising electricity prices always harbour political risks. However, today’s electricity boom is being paid for by financially strong companies such as Google, Meta and Amazon. Regulators are called upon to take the right steps. Then electricity costs for all market participants can be stabilised, if not reduced.

Structural growth in the electricity sector offers further lucrative opportunities for investors.

It will take some time for market participants to realise what this structural change means for investments in the electricity sector.

|

Andreas Schneller is a partner at de Pury Pictet Turrettini & Cie SA and responsible for the ENETIA funds. He is portfolio manager of the ENETIA Energy Infrastructure Fund.

He has managed the fund since 2003. Since 2006, he has been co-portfolio manager of the ENETIA Energy Transition Fund. Mr Schneller has many years of experience in the electricity industry (EIC Partners AG and ABB). He studied business administration in St. Gallen and completed his CEMS Master’s degree at NHH in Bergen (Norway). He is a CFA charterholder. |